Real-world support of the concept of diversity in films. Update 4/12/2026:

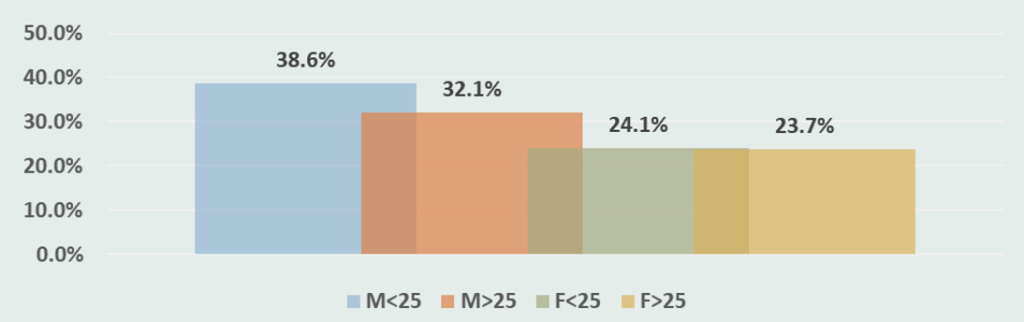

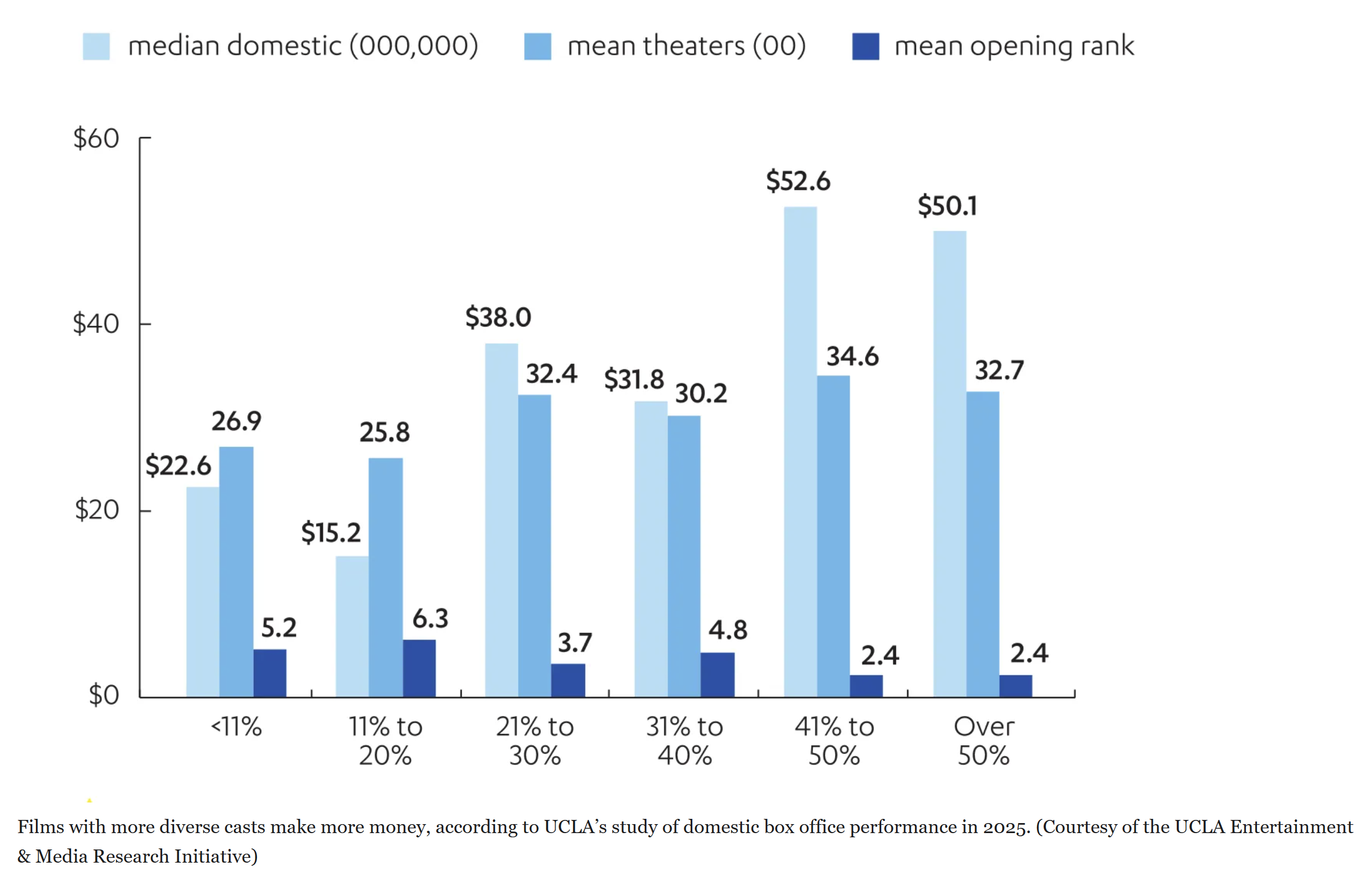

“Domestic Film Performance by BIPOC Cast Share”

In an increasingly and incredibly diverse world, film stories and the people who are in these stories need to be diverse as well. When right for the story, it is right for the distribution stream and for the audience. Studies I consult show me that audiences want authentic stories with authentic characters that reflect their real lives.

I work on films from across the spectrum so I study the attitudes, hopes and desires of a range of people. I enjoy that, and I constantly learn from it. In working on one film, I was learning about what kinds of films contemporary African Americans most like to see. A Morning Consult study and story helped me understand better, and helped me position the film I was working on as having great relevance to these contemporary audiences. Having relevancy to audiences is like injecting value into your film.

Here is a peek at that study:

In politics, this would be well more than a landslide opinion, a move of 18 points. So, I say, diversity in casting, when right for the part (and it is increasingly right for the part) is a boon to a film, and can be a boon to the marketability of your film. Authenticity in your story, in your playing and capturing of the script, authenticity in your marketing are a great way to go.

Here’s me talking about it a little bit in a discussion. (for some unknown reason, Microsoft Edge may not show the video. go here: https://www.youtube.com/watch?v=vuYssxxNRX4)